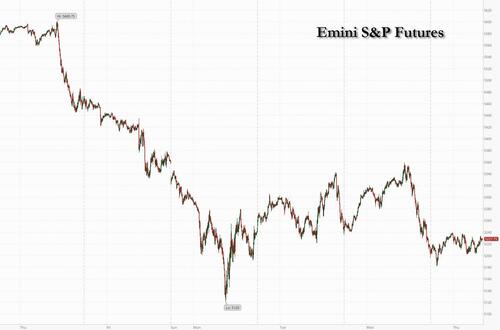

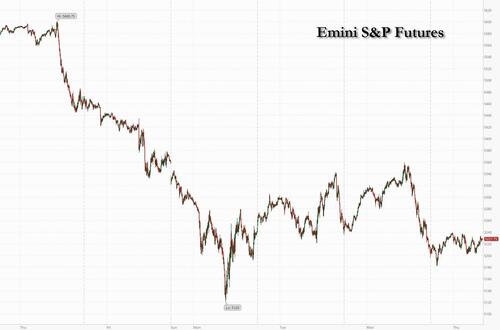

Futures Rebound From Overnight Lows As Sentiment Remains On Edge

After three rollercoaster days of wild, brutal swings, futures are flat ahead of the Thursday open, erasing overnight losses if still below the all-important CTA threshold level of 5255 which trigger billions in sales by systematic funds. Asian and European stocks declined, prolonging the soaring volatility that has gripped global markets for days after the BOJ effectively steamrolled the carry trade last week when it unexpectedly hiked rates, only to U-turn just days later when the Nikkei suffered its biggest one day crash since Black Monday. As of 7:4am S&P futures were unchanged at 5,228 while Nasdaq futures were fractionally in the green, with Mag7 and semis providing support despite the continued selling by Supermicro. Treasuries yields are lower ahead of US jobless claims data, with US 10-year yields falling 2bps to 3.93% as European bonds also gain. Keep an eye on bonds as yesterday’s 10Y auction was weak but that could have been negatively impacted by elevated Credit issuance; today is the 30Y auction. The USD is weaker and commodities are lower across all 3 complexes as WTI dips below $75, but precious metals catch a bid. Today’s macro data focus is on jobless claims; a spike there preceded a weaker NFP that coincided with the carry unwind so the market may have heightened sensitivity to the print. Elsewhere, both Goldman and JPMorgan raised their recession odds, from 10% to 25% and from 25% to 35%, respectively.

In premarket trading, Warner Bros shares plunged after the parent of CNN and TNT posted a $9.1 billion charge write-down on the value of its traditional TV networks. Monster Beverage shares slid after the energy-drink maker missed second-quarter profit estimates. Here are all the notable premarket movers:

- Amneal rises 6% after the drug maker received US FDA approval for its extended-release capsules for the treatment of Parkinson’s Disease, named Crexont.

- Bumble plunges 41% after the dating company slashed its annual revenue outlook, suggesting that an overhaul of the brand’s flagship app has failed to meaningfully reignite growth.

- Dutch Bros slumps 22% after the drive-through coffee chain tempered its store growth outlook.

- Lilly rises 10% after lifting its 2024 sales outlook for the second time this year as its blockbuster weight-loss drug Zepbound outsold expectations.

- JFrog sinks 26% after the application software company cut its full-year forecast.

- Klaviyo jumps 18% after the company boosted its revenue guidance for the year.

- Monster Beverage falls 8% after growth in the energy-drink maker’s revenue and drink volumes slowed to its worst rate since the start of the Covid-19 pandemic.

- SolarEdge tumbles 15% after the renewable energy firm’s revenue forecast for the 3Q came in well below the average analyst estimate.

- Under Armour rises 7% as management raised its guidance as the sports gear brand restructures under returning founder Kevin Plank.

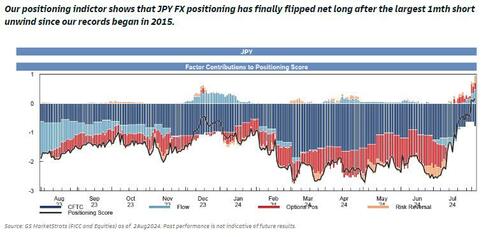

Markets have been extremely volatile since poor jobs data last week fueled worries that Federal Reserve policy is risking a deeper slowdown. Coupled with a rate hike by the BOJ, the carry trade has suffered a historic unwind which according to JPM is about 75% done. Thursday’s US jobless claims figures are in sharper focus than ever after last week’s flimsy payrolls numbers. Investors are also bracing for the US and Japanese central banks to potentially move interest rates in opposite directions in the coming months, putting further strain on the yen-funded carry trade.

This is a “consolidation period before any new trend, given how volatile the market has been,” said Kerry Goh, chief investment officer at Kamet Capital Partners Pte. “Investors probably will stay sidelined until new data appear. The next couple of days will be crucial — either calm returns, or we see a new bout of volatility emerge.”

Meanwhile, as discussed last night, the divergence in US and Japanese central bank monetary policy is set to undermine the yen’s role as a cheap source of funding for financial assets. A Thursday summary of the minutes from last week’s Bank of Japan meeting showed that authorities didn’t see last months surprise rate hike as policy tightening. However, just days later, and following an epic Japanese stock rout, Deputy Governor Shinichi Uchida yesterday said the BOJ won’t raise interest rates when financial markets are unstable, a reassurance that helped buoy stocks and sent the yen lower.

Three-quarters of the carry trade has been unwound as the recent slump wiped out all positive year-to-date returns, according to strategists at JPMorgan while Goldman analysts believe that positioning in the yen is now net long, suggesting most of the carry trade has been unwound.

The carry strategy, which involves borrowing at low rates to fund purchases in higher-yielding assets elsewhere, has been wobbling for months. Carry trades were pummeled over the past week as global market volatility jumped amid fears of rapid Fed rate cuts and after the Bank of Japan’s larger than expected rate hike. The unspooling of the carry trade has further room to run, according to Quincy Krosby at LPL Financial. “A softer dollar, driven by the market’s perception that the Fed will soon initiate an easing cycle, should help support a stronger yen — a negative for the trade.”

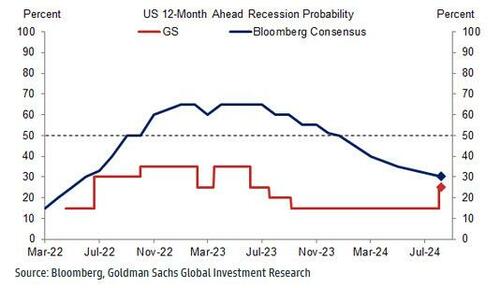

Elsewhere, debate about the path of the US economy continues. JPMorgan now sees a 35% chance that the US economy tips into a recession by the end of this year, up from 25% as of the start of last month. The bank’s new calculation for recession risks followed just hours after a similar step by Goldman, which now sees a 25% probability of a recession in the next year.

Other investors, however, argue that the data still point to a soft landing. “I’m not that worried for the US economy. Yes, unemployment is a concern but it’s not dramatic, it’s just a slowdown,” said Francois Rimeu, a strategist at La Francaise Asset Management in Paris. “I take the view that this was just a volatility episode like we’ve experienced in the past during the summer.”

Europe’s Stoxx 600 index reversed much of Wednesday’s advance, dragged lower by technology and mining shares. The is Estoxx 50 down 1%, tech and industrials underperforming. Siemens shares dropped after the manufacturer said it sees group revenue growth and returns in its key industrial unit at the lower end of forecasts. Zurich Insurance Group AG shares fell after the company reported a rise in losses atit property and casualty arm, driven in part by “higher catastrophe losses and weather events.” Allianz SE climbed after second-quarter profit rose on stronger earnings from its life-health insurance and asset management businesses. Deliveroo Plc rallied after reporting stronger customer orders and saying earnings for the year will be on the higher end of its forecast. Entain Plc soared after the UK gambling firm got an earnings boost from this summer’s European Football Championship.

Earlier in the session, Asian equities first rose but eventually dropped, halting a two-day rally, as Japanese shares reversed an early gain after a volatile trading session. The MSCI Asia Pacific Index fell as much as 0.9%, weighed by tech shares including TSMC, Samsung and Keyence. Japan’s Topix Index declined, as technology firms tracked their US peers lower. Exporters also took a hit after the yen strengthened against the dollar. Benchmarks retreated in Taiwan, South Korea and Australia. Chinese stocks in Hong Kong and the mainland were broadly steady amid the selloff in Asia, burnishing the markets’ appeal as a foil to the ongoing global volatility while investors seek value. Sentiment in the region remained fragile in one of the most tumultuous weeks for stocks in recent memory. The Asian gauge is headed for its fourth successive week of losses as investors reassess the outlook for the US economy and the nation’s interest rate trajectory.

In FX, the Bloomberg Dollar Spot Index falls 0.2%. The Swiss franc tops G-10 peers and the Japanese yen also rises in a haven bid. The Australian dollar climbs after more hawkish rhetoric from the RBA.

In rates, Treasuries hold small gains in early US trading. Yields are richer by 1bp-2bp across the curve with inverted 2s10s around -3.5bp after closing at YTD high -2.1bp Wednesday; new 10-year is around 3.93%, lagging bunds in the sector and outperforming gilts. Supply remains in focus as auction cycle concludes with $25b 30-year bond sale and at least a couple of corporate offerings are expected to follow Wednesday’s deluge of almost $32 billion. Yesterday’s unexpectedly weak 10Y auction which tailed by 3.1bp, a notably poor result, as it drew the lowest yield in a year and spooked markets and precipitated a cross-asset selloff. The When Issued on the 30-year yield is at ~4.225% is ~17bp richer than last month’s, which tailed by 2.2bp

In commodities, oil steadied after its biggest advance in a week, with traders still glued to fluctuations in wider markets and tensions in the Middle East. Spot gold rises $13 to around $2,396/oz.

Bitcoin rises 3.7% after Ripple framed the recent SEC ruling as a win for the company.

Looking at today’s calendar, US economic data slate includes weekly initial jobless claims (8:30am) and June wholesale inventories (10am). Scheduled Fed speakers include Barkin at 3pm

Market Snapshot

- S&P 500 futures up 0.1% to 5,231

- STOXX Europe 600 down 1.1% to 490.56

- MXAP down 0.3% to 173.35

- MXAPJ down 0.4% to 544.49

- Nikkei down 0.7% to 34,831.15

- Topix down 1.1% to 2,461.70

- Hang Seng Index little changed at 16,891.83

- Shanghai Composite little changed at 2,869.90

- Sensex down 0.6% to 79,019.95

- Australia S&P/ASX 200 down 0.2% to 7,681.98

- Kospi down 0.5% to 2,556.73

- Brent Futures down 0.4% to $78.02/bbl

- Gold spot up 0.5% to $2,394.27

- US Dollar Index down 0.21% to 102.98

- German 10Y yield -3 bps at 2.24%

- Euro up 0.1% to $1.0938

Top Overnight News

- BOJ summary of opinions shows the central bank discussed further rate hikes at last month’s meeting, but officials also believe policy remains accommodative despite modest tightening measures. RTRS

- China’s regional banks are under fresh scrutiny from regulators for snapping up treasury notes amid an extended rally in Chinese government bonds that’s drawn alarm from the central bank. WSJ

- The PBOC may have more room for rate cuts if the Fed eases aggressively. Some economists say China’s surprise cut last month could now be followed by another two such moves in 2024 — easing on a scale unseen in years. BBG

- Taylor Swift has cancelled three concerts in Vienna after Austrian authorities said they had uncovered an Islamist terror plot to attack the singer-songwriter’s fans in the city this week. Austrian police arrested a 19-year-old Austrian citizen on Wednesday morning and a second individual of undisclosed age and nationality in the afternoon. FT

- Italy has doubled a flat tax on the foreign income of new residents, in a blow to rich expats seeking to flee the prospect of higher levies elsewhere in Europe. Prime Minister Giorgia Meloni’s cabinet on Wednesday approved a rise in the annual levy on overseas income for new tax residents in Italy to €200,000. FT

- US consumers are reining in spending on travel and leisure, hitting businesses including Disney theme parks, Airbnb home rentals and Hilton hotels as questions grow about the health of the economy. FT

- Major cryptocurrencies ticked upward after Ripple was ordered by a US court to pay a $125 million penalty, just a fraction of what the SEC had sought. “The SEC’s headwinds against the whole of the XRP community are gone,” Ripple CEO Brad Garlinghouse said on X. BBG

- Ukraine launched rocket and drone attacks as its forces expanded their operation inside Russia’s Kursk region, on the second day of a bold incursion that has forced Moscow to redeploy troops from the Ukrainian front. FT

- Google and Meta made a secret deal to target advertisements for Instagram to teenagers on YouTube, skirting the search company’s own rules for how minors are treated online. FT

A more detailed look at global markets courtesy of Newsquawk

APAC stocks traded mixed after the weak handover from Wall St where the major indices fumbled early gains and finished in the red amid soft earnings and geopolitical risks. ASX 200 was dragged lower amid underperformance in the commodity-related stocks including BHP which is reportedly planning to sell Brazilian copper and gold assets it acquired in the takeover of Oz Minerals. Nikkei 225 slumped in early trade with losses of as much as 2.5% before briefly staging a full recovery. Hang Seng and Shanghai Comp. pared opening losses with the former making its way back towards the psychological 17,000 level, while the mainland also pared early losses but kept within a narrow range amid light catalysts.

Top Asian News

- BoJ Summary of Opinions from the July 30th-31st meeting stated one member said they must be mindful of upside risks to inflation and a member said a tight labour market and rise in import prices from a weak yen will likely keep inflation under upward pressure. There was also the opinion that it is appropriate to raise the interest rate given that the economy and prices are moving in line with forecasts and there is a need for vigilance to upside inflation risk. Furthermore, a member said there is no change to the fact that the BoJ is supporting the economy even upon raising rates as a nominal rate of 0.25% is very accommodative, while one member said given the environment surrounding inflation, it is good time to consider small rate hike and a member also said the BoJ should eventually raise rates to levels deemed neutral to economy, which is likely at least around 1%.

- RBA Governor Bullock said they are vigilant to inflation risks and will not hesitate to hike if needed, while she added the board considered a hike on Tuesday and current rates are still deemed to meet the inflation mandate. Bullock said core inflation is not expected to return to the 2–3% target range until the end of 2025 and based on current information, the RBA does not anticipate rates coming down quickly. Furthermore, she said the RBA does not react to individual economic numbers and if the economy declines faster than expected, the RBA would consider cutting rates but sees the need for more evidence to alternate the rate stance.

- RBI kept the Repurchase Rate unchanged at 6.50%, as expected, while it maintained the stance of remaining focused on the withdrawal of accommodation in which 4 out of 6 members voted in favour of the rate decision and policy stance. RBI Governor Das said India’s growth remains strong and inflation is broadly on a declining trajectory. Furthermore, Das said they want inflation to progressively align with the target and noted the food component of inflation remains stubborn but added that going forward, the base effect on inflation will wear out.

- Earthquake in Japan’s southern region, prelim. magnitude of 6.9 (rev. to 7.1 at 08:57BST), via NHK; Tsunami warning has been issued for Miyazaki and Kochi, then broadened to Kagoshima and Ehime

European bourses are lower across the board, Euro Stoxx 50 -1.2%, as the downbeat sentiment from Wall St. reverberated into APAC trade and continued. Macro newsflow light, earnings driving sectoral differences with Travel & Leisure underpinned by Entain numbers, Telecoms supported by Deutsche Telekom. Stateside, US futures are lower across the board but only modestly so with losses shallow than those seen in Europe, ES -0.4% & NQ -0.3%. Ahead, a handful of earnings due.

Top European News

- Turkey Keeps Year-End Inflation Outlook on Slowing Demand

- Siemens to Hit Low End of Forecasts on Slow Automation Sales

- Duerr Surges on Earnings Beat and Improved Order Intake Outlook

- Deliveroo Orders Grow as Demand Picks Up Across Markets

- Turkish Central Bank Keeps Year-End Inflation Outlook Unchanged

- Anti-Racism Protesters Give UK Respite After Days of Riots

FX

- DXY is softer intraday after mild gains on Wednesday, with a lack of specific catalysts thus far into US data and supply; holding just 103.00.

- JPY unreactive to a Japanese earthquake and tsunami; USD/JPY just above the 146.00 mark and softer on the session with overall action much more contained than that seen recently.

- EUR underpinned by the mentioned soft USD, but only modestly so with specifics light; similar story for Sterling, though Cable has slipped below the 1.2700 mark.

- Antipodeans are firmer, outperformance once again for the AUD after comments from the RBA Governor. Kiwi kept afloat despite softer inflation expectations which have increased the odds of an RBNZ cut next week.

- PBoC set USD/CNY mid-point at 7.1460 vs exp. 7.1821 (prev. 7.1386).

Fixed Income

- Fixed benchmarks bid, specific drivers light and the action overall well within recent parameters.

- Complex is essentially in a holding pattern ahead of US weekly data and then a 30yr auction which follows the soft 10yr on Wednesday.

- Bunds at the mid-point of c. 50 tick parameters with Gilts in-fitting but in even narrow ranges while USTs are inching toward Wednesday’s 113-37 best having pared the late-doors auction-driven downside.

Commodities

- Crude is subdued but holds onto the bulk of yesterday’s gains, complex is focussed on geopols as we await a Iran/Lebanon retaliatory strike against Israel with potential Hezbollah action also a point of focus.

- WTI Sep trades within a USD 74.78-75.70/bbl range while Brent Oct trades within a USD 77.80-78.70/bbl band.

- Nat Gas benchmarks began with marked gains, bolstered by reports of Ukrainian troops launching an attack on the Kursk, Russia region; however, the situation in Kursk has, according to somewhat mixed Russian reporting, seemingly stabilised a touch and has caused a pullback from best.

- Metals are mixed, precious peers supported by the geopolitical landscape but in narrow ranges while base metals are near-unchanged, though LME Copper attempting to pare some of Wednesday’s hefty pressure.

- Russia’s Gazprom is continuing shipping gas to Europe via Ukraine, Thursday’s volume at 37.3MCM (prev. 39.4MCM on Wednesday and 42.3MCM on Tuesday).

- China’s NDRC to cut the retail gasoline and diesel price by CNY 305/T and CNY 290/T respectively as of 8th August.

Geopolitics: Middle East

- Iran’s UN envoy said Tehran’s “priority is to punish the aggressors” responsible for Haniyeh’s assassination in Tehran and preventing the repetition of terrorist attacks by Israel. This follows a report that US officials said Iran may be rethinking launching a multi-pronged attack on Israel, while they do anticipate an Iranian response to the Haniyeh killing but think Tehran seems to have recalibrated and the US does not expect an imminent attack.

- Hezbollah reportedly looks increasingly like it may strike Israel independent of whatever Iran may intend to do, according to two sources familiar with the intelligence cited by CNN.

- Israeli officials think the target for Hezbollah’s response could be the IDF headquarters in the centre of Tel Aviv or the Mossad headquarters and other key intelligence bases in northern Tel Aviv, according to Axios’s Ravid.

- Israel told the US if Hezbollah harms Israeli civilians as part of its retaliation for the assassination of its top military commander, the Israel Defense Force’s response would be disproportionate, according to two officials cited by Axios.

- Saudi Deputy Foreign Minister said Haniyeh’s assassination is considered a 'blatant violation’ of Iran’s sovereignty.

Geopolitics: Other

- Russia’s Medvedev said Russia must press on to Odesa, Kharkiv, Dnipro, Mykolaiv, Kyiv, and further, while he added that Russia will stop only when it finds it acceptable and beneficial.

- Russia’s Defence Ministry says Russia is thwarting Ukraine attempts to break through deeper into Russia’s Kursk region, according to agencies.

US Event Calendar

- 08:30: July Continuing Claims, est. 1.87m, prior 1.88m

- 08:30: Aug. Initial Jobless Claims, est. 240,000, prior 249,000

- 10:00: June Wholesale Trade Sales MoM, est. 0.3%, prior 0.4%

- 10:00: June Wholesale Inventories MoM, est. 0.2%, prior 0.2%

- 15:00: Fed’s Barkin Speaks in Fireside Chat

Tyler Durden

Thu, 08/08/2024 – 08:10

![Zełenski odsyła order, Ormuz ponownie zamknięty [SKRÓT DNIA]](https://v.wpimg.pl/MDc0ZWJiYiUCUixkZRJvMEEKeD4jS2FmFhJgdWVYf3BTSG1hekYrLQ9VKDI6BmMjEUUqNj0ZYzQPHzsnI0Y7dUxUMyQ6BSw9TFU3NS8NYnVbAT40K1kraVJUY2FnXS53Ah1jNigLYH1aB2pgfgwvJlJRP3U3)